A majority of Americans are in debt. Maybe that statement doesn’t surprise you, because chances are that you’re part of that majority. There’s a reason I say that, and it’s not that I’m just trying to generalize.

The fact of the matter is that 77% of American households have some kind of debt. But just how much do these households owe? Let’s put some dollar figures to that statistic.

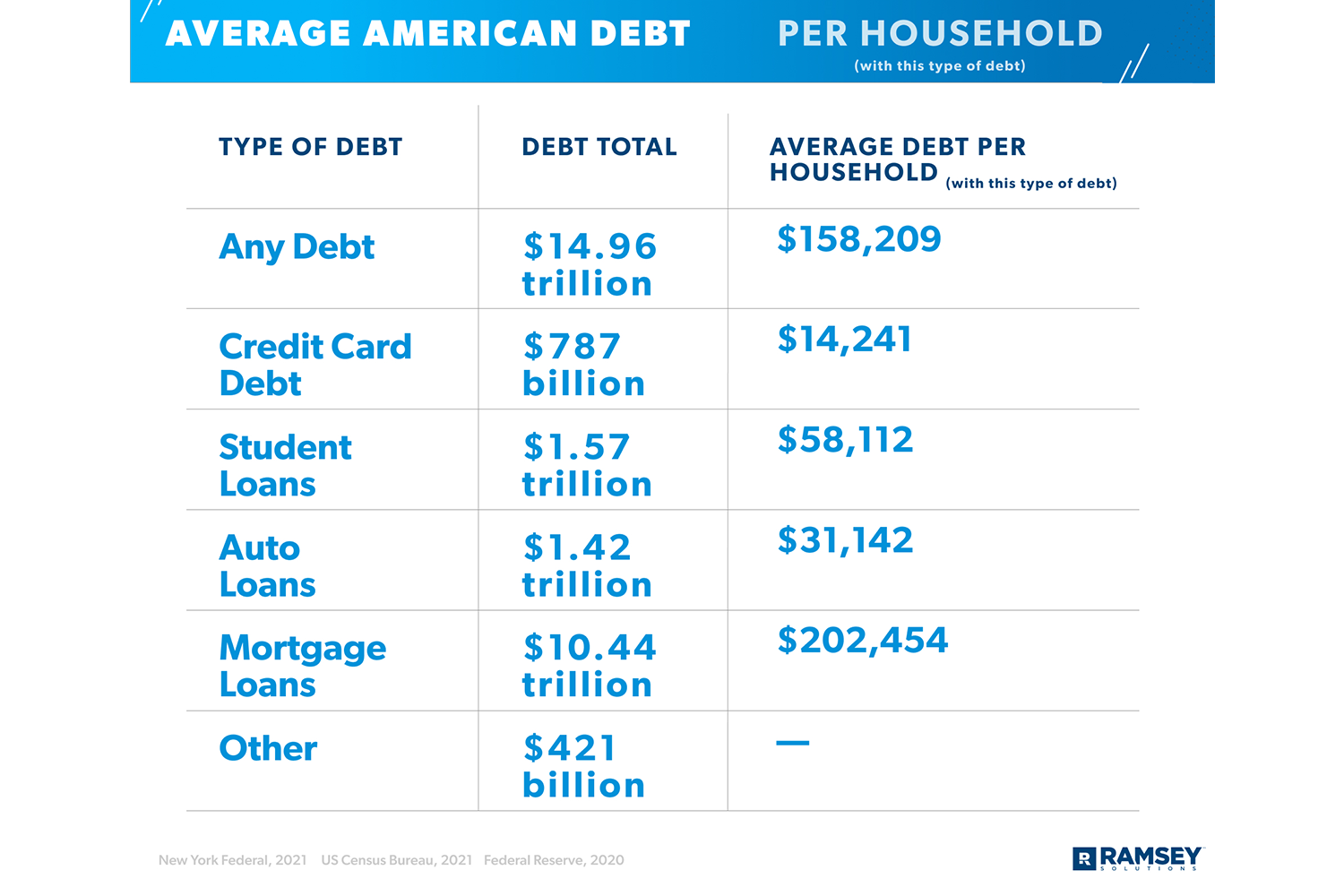

The total of any debt in the United States is $14.96 trillion . According to Ramsay Solutions, this is an average of $158,209 per household. Mortgage loans make up the majority of debt, followed by student loans, then auto loans, and finally credit card debt. There are other costs as well, but these are the most common.

Of course, people can manage these by making consistent payments to the organization they owe. For instance, homeowners make monthly mortgage payments to their lenders.

These bills become problematic when the borrower misses a payment or stops making them altogether. No one wants to end up in that situation, but the reality is that it can be hard to keep up with too many payments. This results in one-quarter of Americans who don’t pay their bills on time.

Enter: debt collectors. If you’re reading this blog, then you most likely know what these people do. You might even be one yourself.

But just in case you stumbled here looking for the definition, let me summarize. Debt collectors do exactly what it sounds like they do…collect debts. If a borrower doesn’t pay their bill, then the collector buys these past-due payments from the business or creditor. They then try to collect what the person owes.

To do this, they send debt collection letters. Put simply, these remind an individual that they owe money. The goal is that the person will finally pay, especially now that their bill is in the hands of a collection agency. After all, no one wants to deal with any potential legal action.

I’m sure you can agree. Even as a debt collector, you don’t want to handle potential lawsuits. But how do you get people to pay before it gets to that point?

Writing an effective yet ethical letter is the first step to initiating this process. You might be wondering what exactly I mean by “ethical.” It’s more than just writing a polite letter . As a debt collector, there are legal requirements that you need to follow.

If I had to guess, most people aren’t missing their payments simply because they don’t feel like paying. A more probable reason is that they have financial difficulties making it impossible to afford. Because it’s a sensitive situation, the government offers protections for people when it comes to collection agencies’ attempts to get their money.

The Fair Debt Collection Practices Act protects individuals from inappropriate and abusive behavior from debt collectors. This law states that collectors can’t …

There’s a movie from 2009 called Confessions of a Shopaholic . The main character, Rebecca Bloomwood, owes a debt collector thousands of dollars. The collector, Derek Smeath, violates so many of these rules. He harasses her by repeatedly calling her personal and work phone, and he shows up at her apartment and place of work.

In one scene, Bloomwood is a guest on a talk show on live television. She doesn’t know that Smeath is in the audience. When the talk show host asks the audience for questions, he exposes Bloomwood’s debts in front of the entire audience and on live television.

Of course, the film is a comedy so they don’t focus on how he was breaking so many rules that the FDCPA would have protected her from. But it’s a good example of what collection agencies shouldn’t do.

So now that you know the ethics behind contacting those who owe money, here are four effective debt collection letter examples that you can use.